Pete Wargent BlogSpot| 13 September 2019

https://petewargent.blogspot.com/2019/09/whats-happening-with-lending-standards.html

A bit of interesting chit-chat on the Twitter today concerning whether mortgage lending standards are looser, or tighter…or neither of the above.

On the one hand, the minimum assessment rate for mortgages was lifted, and replaced by a minimum 250 basis points buffer as I looked at previously here (while previous caps on investor and interest-only loans no longer apply).

That may represent at least a theoretical increase in borrowing capacity for some borrowers, especially where the loan is written at around a 4½ per cent mortgage rate or lower.

On the other hand, however, banks are taking a much keener interest in actual household expenses than I’ve ever experienced or heard of before – in Australia or overseas – so from that perspective credit standards are as high as they’ve ever been.

Net net…no real loosening.

Rather, there’s just been an overdue resurgence of homebuyers as those procrastinating in the lead-up to the election have finally returned, and hopefully established stock turnover will now bounce from two-decade lows.

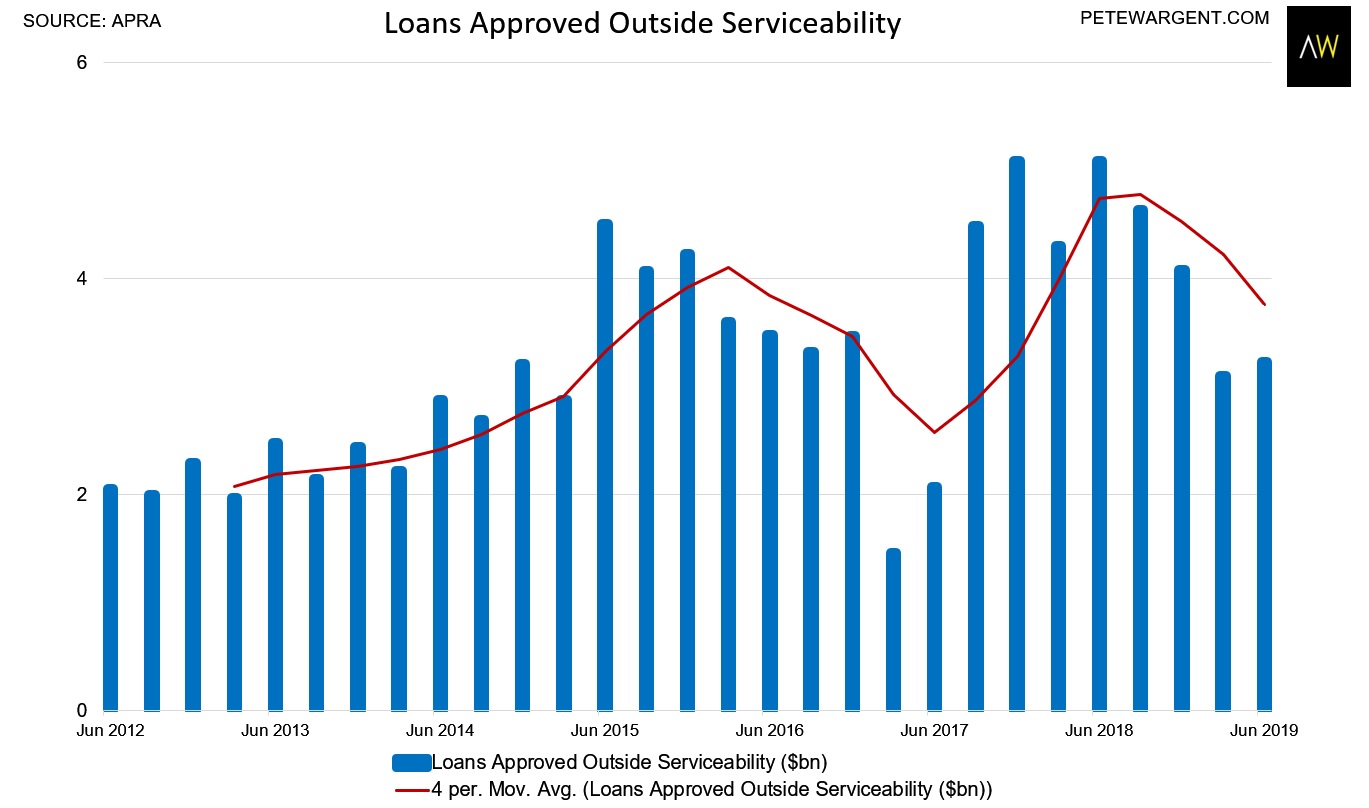

Some commentary examines loans approved outside serviceability as a proxy for marginal lending behaviour.

I’m not sure if you can draw strong conclusions, except to observe that some loans in the pipeline might be flagged as an exception during period of tightening (hence the jump after restrictions were put in place in 2017).

For completeness, loans reported as outside serviceability have declined at major banks, partly offset by an increase at mutuals as the smaller players jockey for market share.

There have already been the predictable calls to reintroduce macroprudential measures after a modest rebound in lending.

But generally speaking, overall lending procedures are now very robust (if not too pedantic, at times).