Phillip Coorey| Australian Financial Review| 14 October 2019

https://www.afr.com/politics/federal/big-banks-face-new-accc-pricing-probe-20191013-p5307r

Treasurer Josh Frydenberg has charged the consumer watchdog with investigating the refusal of the banks to pass on in full the recent spate of interest rate cuts, creating the potential for a further round of government intervention.

After his calls for the banks to pass on rate cuts in full were ignored for a third time this year, Mr Frydenberg tasked the Australian Competition and Consumer Commission with looking into the pricing of residential mortgage products, and to examine obstacles that stop customers switching lenders.

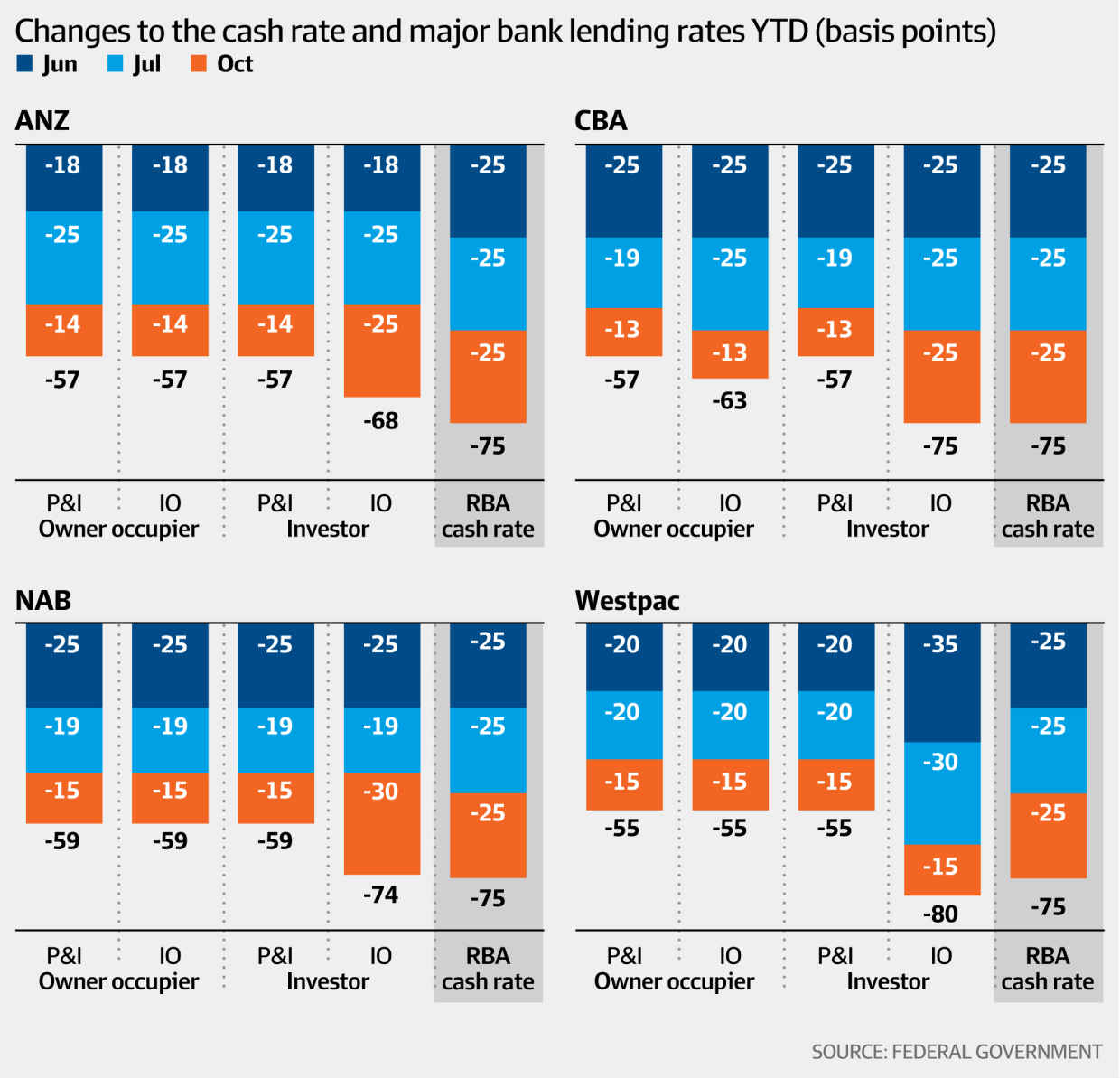

The ACCC will focus on the period since January this year and the response by the banks to the three rate cuts made by the Reserve Bank in June, July and October, which have resulted in the cash rate being reduced by a total of 75 basis points.

At the same time, the big four banks have passed on an average of 57 basis points in owner-occupied home loan rates.

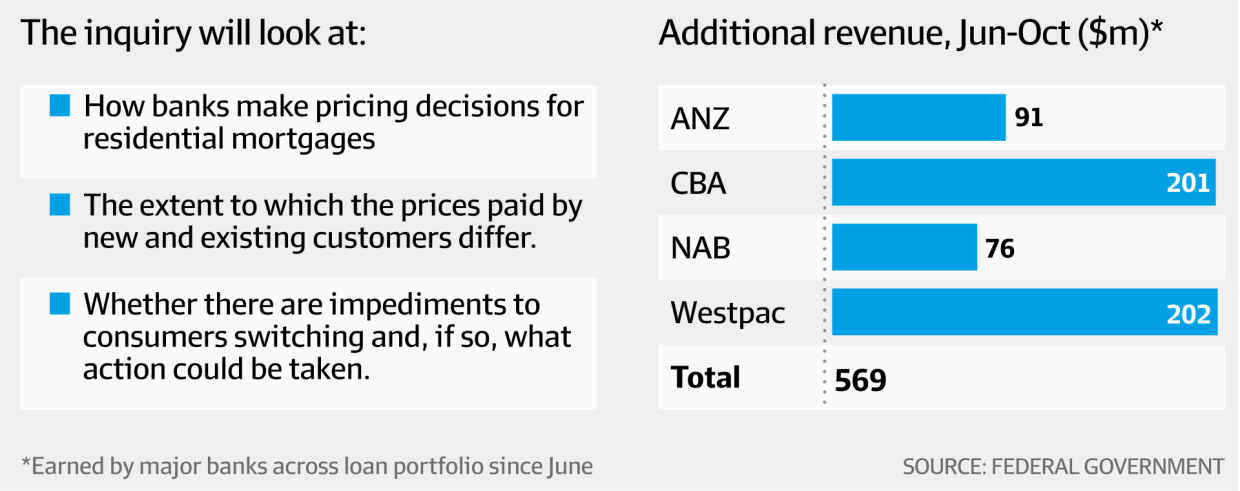

Their refusal to pass the rate on in full, as well as delays in passing on the reductions the banks did grant, will see the big four pocket $569 million in revenue between them, according to Treasury numbers released by Mr Frydenberg.

The inquiry will focus on the entire residential mortgage sector – the big banks, the smaller banks and non-bank lenders – but the emphasis will be on the big four, which have 75 per cent of the market.

It comes after ACCC chairman Rod Sims accused banks of dudding their loyal customers, a claim rejected by RBA member Ian Harper who countered that price discrimination was neither illegal nor unusual.

The actions of the big banks in not passing on the cuts in full have not only embarrassed the government but have limited the effect of the RBA cuts in terms of providing economic stimulus.

Related

Higher interest rates would hurt economy

RBA governor Philip Lowe has asked they be passed on in full, as has the Treasurer.

“The failure of the banks to fully pass on the recent rate cuts to their customers when their cost of funds have come down significantly, leaves them exposed to the charge that they are putting their profits before their customers,” Mr Frydenberg said.

“This is not a good outcome for either their customers or the economy as a whole, and comes just months after the royal commission shone a bright light on misconduct in the banking sector.

“With this new inquiry, the government is providing the banks with an opportunity to transparently account for their decision-making and how they balance the needs of borrowers, savers, shareholders and the wider community.

“The information gathered by the ACCC using their special powers will help inform policy makers as we seek to get customers the best possible deal from their bank.”

Three areas of focus

The inquiry would concentrate on three key areas. The first of these would be how banks make their pricing decisions when setting residential mortgage rates, including their response to official movements in the cash rate. This will take into account such factors as the bank’s borrowing costs and their profit margins.

Secondly, it will look at whether customers are being gouged by the so-called “loyalty tax” by assessing the extent to which the prices paid by new and existing customers differ, as well as the difference between the reference interest rates published by suppliers and the interest rates paid by customers.

Thirdly, it will consider the impediments that discourage people from switching banks and what action could be taken to reduce these impediments.

The inquiry will deliver its findings on pricing decisions related to rate cuts as well as the “loyalty tax” on March 30, next year. This creates the potential for response measures to be announced on or before the May budget.

It also heaps pressure on the banks to pass on in full the next rate cut, which the RBA hinted, when it last cuts rates, could be as early as Melbourne Cup Day.

The ACCC’s findings into impediments to switching banks will be in the final report due September 30.

In 2010, then-Labor treasurer Wayne Swan announced a comprehensive package of measures to help people switch banks which included banning exit fees on new mortgages, boosting consumer flexibility to transfer deposits and mortgages, and empowering the smaller banks so they could compete better with their bigger counterparts.

No rise in bank levy

The Coalition government is already implementing consumer data rights giving customers greater access to their personal information and making it easier to switch banks.

In recent weeks, both Mr Frydenberg and ACCC chairman Rod Sims have effectively accused banks of slugging customers with a “loyalty tax”, which is hitting long-term customers with higher interest rates in the knowledge they won’t switch.

Related

Shop around to beat the banks’ ‘loyalty tax’

The same term was used by the government against power companies, which also relied on customers not having the time or inclination to shop around for a better deal.

Last week, Mr Frydenberg said banks were happy “leaving their existing customers in the cold” to win new business, but stopped short of recommending a default market offer-style mechanism for mortgages, similar to the model introduced into the energy sector to stop providers profiting off customer inertia.

Mr Frydenberg has ruled out any further increase in the bank levy, something Labor flagged when the banks refused to pass on in full the October rate cut.

Shadow treasurer Jim Chalmers called then for a new ACCC inquiry and an increased hike in the bank levy as options.

“We do want our financial system to be as competitive as possible,” he said. “We do want to see those rate cuts passed through so that they can do good, not just in household budgets but in the shops and businesses and in the broader economy as well.”

Mr Chalmers said Labor would not support legislation requiring the banks to pass on the full RBA rate cut.

Mr Frydenberg said the ACCC inquiry was needed on top of the banking royal commission because the commission looked at misconduct in the sector, not the way banks priced their mortgages.

The previous ACCC Residential Mortgage Price Inquiry specifically focused on whether the Bank Levy affected the prices charged for residential mortgages.